HEDGING CONSIDERATIONS

Overview of New Issue Risk Exposures

When issuing a bond there are a number of risks an issuer should consider:

- Floating rate risk – for a floating-rate note (FRN) issuance, an increase in the floating benchmark rate (e.g. USD LIBOR) will result in an increased interest expense for the issuer (i.e. if USD LIBOR increases 1%, the issuer’s interest expense increases by 1%).

- Government benchmark rate risk – for a fixed rate bond issuance priced using a government benchmark rate, an increase in the government benchmark rate from the beginning of the bond issuance process until the issue date will result in an increased interest expense for the issuer (i.e. if the government benchmark rate increases 1% and the issuer’s credit spread remains unchanged, the issuer’s interest expense increases by 1%).

- Currency risk – for bond issuances in currencies other than the issuer’s functional currency, adverse changes in FX rates can increase the issuer’s cost of debt (i.e. if a Canadian dollar functional company issues a U.S. dollar bond, and the Canadian dollar depreciates 20% relative to the U.S. dollar, the issuer’s interest expense and principal repayment has increased by 20%).

Summary of Traditional Derivatives Hedging Tools

To manage risk exposures associated with a bond issuance, an issuer can use one or more of the following derivatives hedging tools:

-

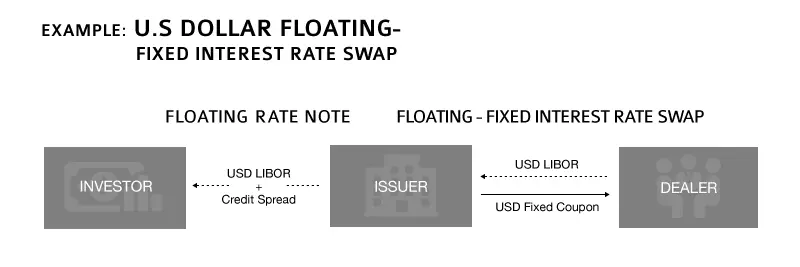

To hedge floating rate risk, an issuer can

use a floating-fixed interest rate swap

The issuer receives a floating rate of interest from the dealer, which offsets the interest due under its floating-rate note. In exchange, the issuer pays the dealer a fixed rate of interest.

-

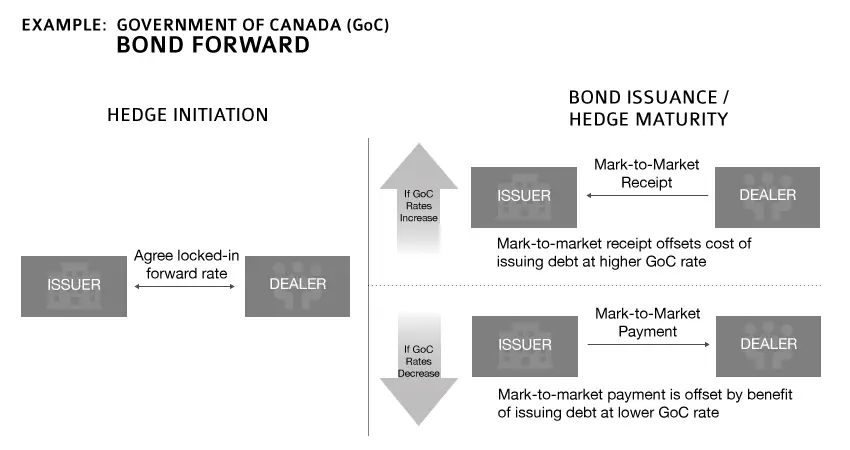

To hedge government benchmark rate risk, an issuer can

use a “bond forward” transaction to effectively lock-in

an underlying government benchmark rate in advance of a new issue.

The issuer sells the government benchmark bond forward, which locks-in the government benchmark rate component of its new issue.

-

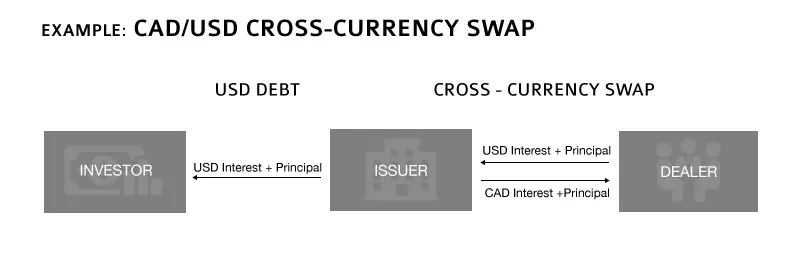

To hedge currency risk, an issuer can use a cross-currency swap

The issuer receives USD interest and principal payments from the dealer, offsetting its USD debt obligation. In exchange, the issuer pays the dealer CAD interest and principal. As a result, the currency risk associated with USD debt is mitigated.

The above strategies are the most “traditional” hedging alternatives for issuers, however, there are many other hedging solutions provided by dealers, including option-based strategies and hybrid structures.