INTEREST & PRINCIPAL REPAYMENT

Repayment Schedules

Fixed income securities are structured to fit an issuer's specific objectives and financial limitations while satisfying market demand. As such, interest and principal repayment schedules of a fixed income security are customized by adjusting one or more of these characteristics:

- Fixed or variable coupon rate – over the life of a fixed income security, it can have either fixed or variable interest payments.

- Principal repayment – fixed income securities can either pay the principal amount in a single settlement at maturity or distribute the principal throughout the security’s life.

- Coupon frequency – interest payment periods may vary from annual to semi-annual to monthly payments.

- Maturity – fixed income securities’ maturities range from a fixed hundred-year maturity to demand features that give investors the daily option to tender their investments. Standard benchmark tenors include 3-year, 5-year, 10-year and 30-year for corporate bonds.

Adjusting any of these characteristics will alter the fixed income securities repayment schedule, price, and investor interest.

The issuer initially receives the $1,000 loan from the investor. At each subsequent period (i.e. 6 months), the issuer will pay the investor a $25 coupon payment until maturity. When the bond matures, the issuer will pay the investor a $25 coupon in addition to the $1000 principal. A non-callable fixed-rate bond is also known as a bullet bond.

Fixed-Rate Bond

Semi-annual pay bonds are the standard form of borrowing in the debt capital market. These bonds pay a fixed coupon rate of interest in two equal semi-annual payments until maturity. Their maturity dates are typically set in advance. The cash flow of this bond is broken down into a series of fixed interest payments and a single principal payment at maturity.

Floating Rate Note

Floating rate notes (FRNs) are variable rate bonds with coupon rates that are tied to a benchmark rate (e.g. 3-month LIBOR). FRN coupon payments are paid monthly, quarterly, semiannually, or annually and reset every period. FRNs are typically between two to five years to maturity, but may be as long as ten years.

Amortized Bond

Amortized bonds, or “amortizers”, are bonds where the principal amount is paid down over the life of the bond along with the coupon payments. An amortized bond’s principal and coupon payments follow an amortization schedule, which typically has equal payments.

Real Return Bonds

Real return bonds (RRBs) are inflation-linked bonds. RRBs’ coupon rates are adjusted for inflation. For example, coupon payments for each period could be linked to the prevailing Consumer Price Index (CPI) at the start of each payment period.

Sinking Fund

A bond can include a sinking fund feature where the issuer makes periodic payments to retire part of the issue by purchasing bonds in the open market. A sinking fund adds safety from the perspective of investors as the likelihood of default due to failure to repay principal is reduced.

ERA OF LOW INTEREST RATES

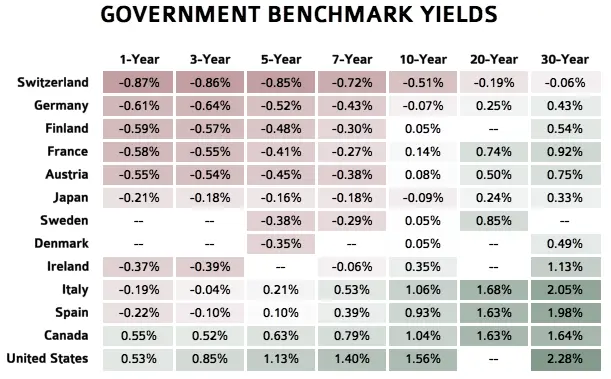

Following the financial crisis of 2008, global interest rates have declined to all-time lows, with sovereign yields in many countries becoming negative – something many economists never believed to be possible. A key driver of the decline comes from central banks globally, that have since 2008, engaged in the most accommodative monetary policy in history. This new era of low interest rates has been popularized by PIMCO as the “new neutral”

(Source: Bloomberg)

The extensive level of monetary policy is best understood through two key pillars:

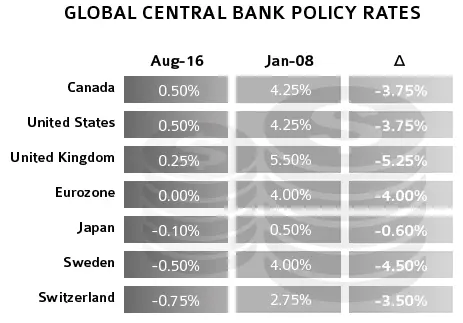

- All time low central bank policy rates – since the financial crisis, central banks have cut policy rates so low that they currently sit at or near historical lows in many developed nations. To better understand central bank policy rates please see here.

- Unprecedented amount of quantitative easing (QE) - as measured by Stratfor, in the U.S. alone, ~$4 trillion of securities were purchased during the country’s QE program. QE has since been ended by the U.S., however, the Eurozone, Japan and the United Kingdom are currently engaged in their own programs. To better understand QE, please click here.

(Source: Bloomberg)

Overall, the extreme decline in interest rates has driven distortions in both fixed income and equities markets and has driven many economists to question previously popular frameworks.