OVERVIEW

Participants in the Fixed Income Market

There are three participants directly involved with the fixed income market: issuers, investors, and dealers. Issuers mandate a syndicate of dealers to underwrite and distribute the bond offering to investors. There also exists other participants who offer essential services to these primary market participants.

Issuer

Issuers raise funds by offering bonds and other debt instruments in the debt capital markets to fund existing operations or invest in new projects. Issuers largely comprise of governments and corporations. Of note, government entities utilize the debt capital markets to fund the majority of public operations. Depending on market conditions and issuer-specific financing needs, corporations will issue debt when it is favorable compared to equity or other funding alternatives.

Dealer

Dealers are financial institutions – predominantly investment banks – that play an important role by helping corporate and government entities make sound financial decisions and raise capital. Dealers provide advisory, underwriting and other services to issuers when they are interested in issuing securities to raise capital. This involves drafting legal documents (e.g. prospectus, term sheet), soliciting interest from investor counterparties, and supporting the price discovery and allocation process. In general, issuers appoint a syndicate of dealers, reducing the financial burden of the deal on the lead by distributing the risk exposure among the syndicate dealers. Dealers provide diversified services to issuers and investors such as research, sales & trading, and structuring.

Other Participants

Other participants provide essential services throughout the debt issuance process. Credit rating agencies assess the issuer’s credit rating, a key indicator of the issuer’s credit health. Legal counsel drafts and files legal documents and provides the issuer with legal advice through the issuing process. Settlement agent is responsible for completing a transaction between a buyer and seller of securities.

ELECTRONIC BOND TRADING

Electronic Bond Trading

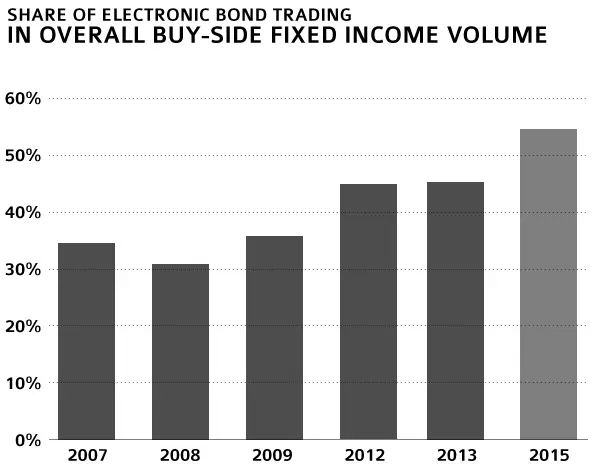

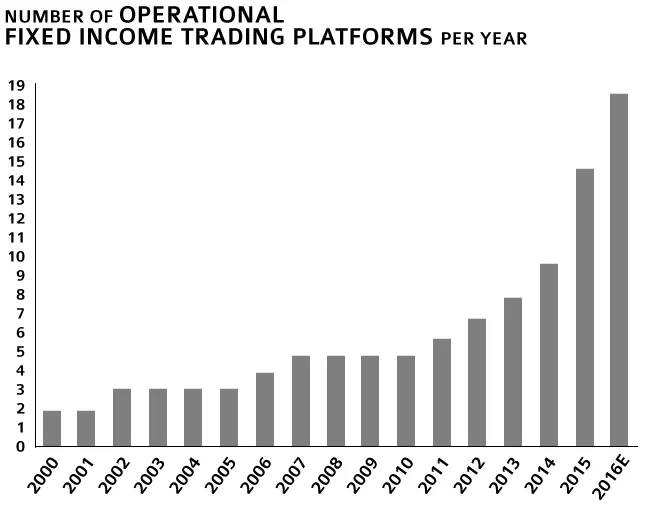

It is evident that electronic trading in the fixed income market has become increasingly prevalent due to the benefits of transparency and liquidity. Although e-trading has not dominated the bond trading markets the way it has on other asset classes (e.g. equities) due to bond’s high heterogeneity, the share of electronic bond trading in buy-side has increased steadily in recent years1. Meanwhile, the number of trading platforms has grown significantly to an estimated of 19 by the end of 2016, compared to only two platforms back in 2000.

Number of Operational Fixed Income Trading Platforms Per Year

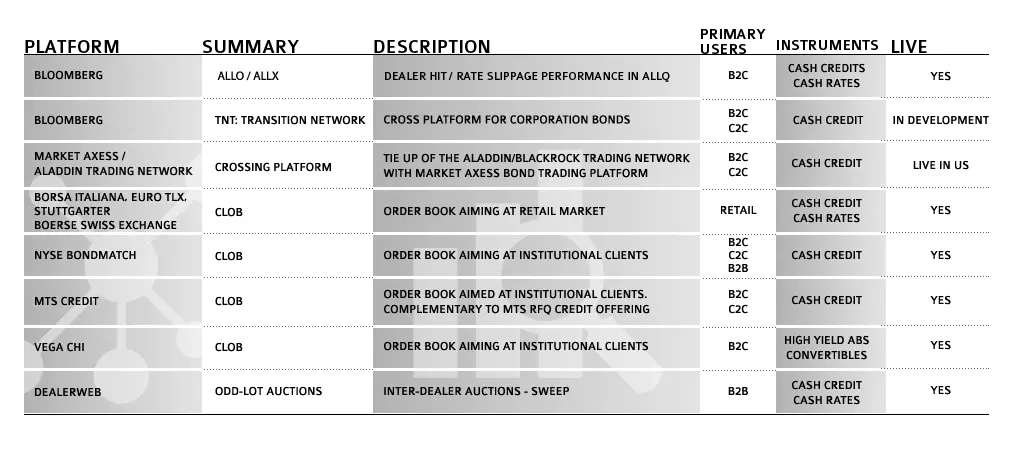

"Fixed income electronic trading platforms are investing in new technologies and finding innovative and creative ways in which to both aid price discovery and to enhance access to market liquidity," said Randy Snook, executive vice president, business policies and practices at SIFMA. In particular, many platforms have increased investment in leveraging technology and data such as standardization of communication protocols to reduce integration costs and to connect market participants more efficiently, pre and post pricing data aggregation to create advanced pricing tools, and enhanced connectivity across technology platforms and trading venues to provide more market liquidity. The table below summarizes commonly used electronic bond trading platforms:

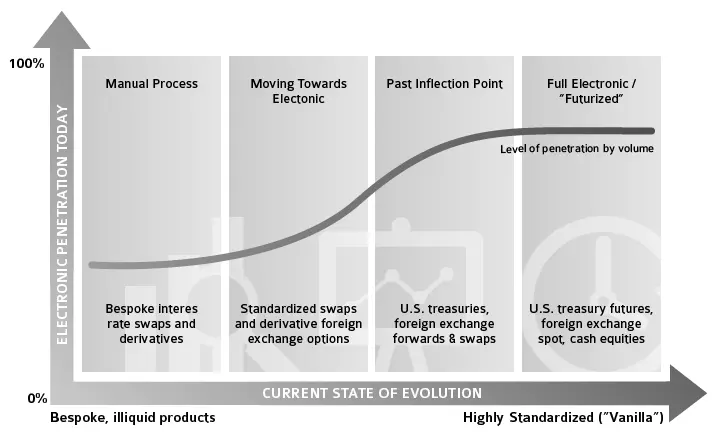

In spite of the fact that “electronification” has increased considerably in bond market trading, it is still in the very early stage compared to other products such as equities or foreign exchanges. However, with increasing digitization and innovation of primary bond markets, it’s likely that electronic penetration in bond markets will further advance in next five years.

References:

- ECB: Electronic Bond Trading Review

- SIFMA: Electronic Bond Trading Report: US Corporate & Municipal Securities

- McKinsey, Greenwich: Corporate Bond E-Trading: Same Game, New Playing Field

IN THE PRESS

"Overbond Ltd., the first end-to-end fixed income markets fintech platform for AI predictive analytics, has launched COBI Pricing, a new proprietary bond pricing and liquidity risk management automation solution. COBI (Corporate and Government Bond Intelligence) is a comprehensive..."

Read More

MARKETS

FX

CAN Rates