BOND INVESTOR RISK CONSIDERATIONS

Overview of Bond Investor Risk Exposures

When investing in a new issue bond there are a number of risks an investor should consider:

- Industry Risk – the risk involved in investing in a specific industry. For example, if oil prices decline significantly, an investment in a corporate bond issued in the oil industry would likely decline in value.

- Economy Risk – the risk of an unforeseen negative change in the macroeconomic environment that adversely impacts the price of a bond investment.

- Country Specific Risk – the risk that changes in a country’s outlook negatively impacts the price of a bond investment. For example, if investing in an emerging market (e.g. Venezuela, Vietnam) and the emerging market declares bankruptcy, corporate bond prices in the country may decline.

- Interest rate risk – as seen here, bond prices and interest rates have an inverse relationship. Thus, a bond investor has risk when interest rates rise and the price of the bond declines.

- Credit spread risk – the risk that the issuer’s credit spread relative to the government benchmark rate increases. As a result, the market rate of interest increases and the price of the bond declines.

- Default risk – the risk that an issuer incurs an event of default and is unable to repay its debt obligations in the future.

-

Call risk – the risk that an issuer

repays (calls) the bonds in advance of the

maturity date. Some bonds have a callable

feature that gives the issuer the option to

redeem the bond at predetermined prices

(call prices) on predetermined dates (call dates)

in the future. Typically, the issuer will exercise

this option if interest rates decline and the price

of the bond rises. Call features create multiple

issues for investors, including:

- Reinvestment risk – as interest rates decrease and the bond is repaid/called, the investor will not be able to invest proceeds at the initial interest rate and must instead invest at the currently low interest rate.

-

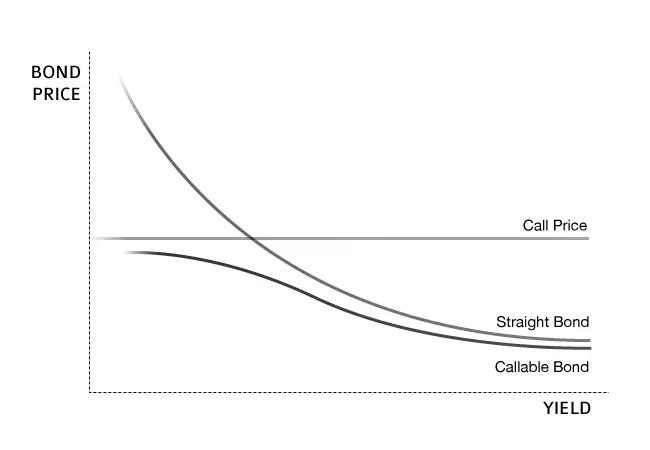

Price compression risk – as interest rates decrease,

there is a higher probability that the issuer calls the

bonds. Due to this, the price of bonds with call features

are effectively capped at the call price (see diagram below).

- Cash flow risk – as it is unknown whether the issuer will call the bond in the future, it can be difficult for investors to develop cash flow plans.

- Liquidity risk – the risk that the investor is unable to liquidate (sell) a bond in the secondary market for fair value due to lack of demand. Typically, if the bond lacks liquidity, an investor will only be able to sell the bond at a discount to the fair value.

- Inflation risk – the risk that the purchasing power of the payments received from the bond investment erode due to an increase in inflation. For example, if the coupon on a bond investment is 3% and the inflation rate is 1%, the real return is 2% (real return = nominal return less inflation rate).

- Currency risk – for bond investments denominated in a foreign currency other than the investor’s functional currency, there is risk that the foreign currency depreciates relative to the functional currency and the value of the bond declines from the investor’s perspective.

-

Event risk – the risk that an issuer

will not be able to make a coupon or principal

payment due to an unexpected event. The most

commons types of event risk are as follows:

- Corporate takeover/restructuring risk – when an issuer’s debt profile changes due to a corporate takeover or restructuring. For example, in a corporate takeover, the firm may take on a significant amount of debt, making it difficult to repay existing debts.

- Regulatory risk – the risk that a change in the regulatory environment adversely affects an issuer’s ability to repay debt.

- Catastrophe risk – a natural disaster (earthquake, hurricane) or industrial accident that limits the issuer’s ability to repay debt.

NOTE ON INFLATION

Market Anomaly - Inflation Expectations

Recently, as of Q3 2016, the derivatives market has begun pricing in low inflation for the foreseeable future. For example, the 50 year U.S. inflation swap rate is currently ~1.88% – indicating that over the next 50 years, the market is approximately expecting an average U.S. inflation rate of 1.88%. This expectation is lower than the historical average U.S. inflation of 3.15% and indicates the market believes there will be less inflation in the future than in the past. This market anomaly may present an opportunity for institutions to hedge inflation risk at historically attractive levels.

Despite all-time low inflation expectations, it is worth acknowledging some structural drivers of lower inflation expectations. On the demand side, aging demographics and the highest levels of debt in history could curb future spending. Conversely, on the supply side, technological innovations could drive lower cost structures for businesses in the future.