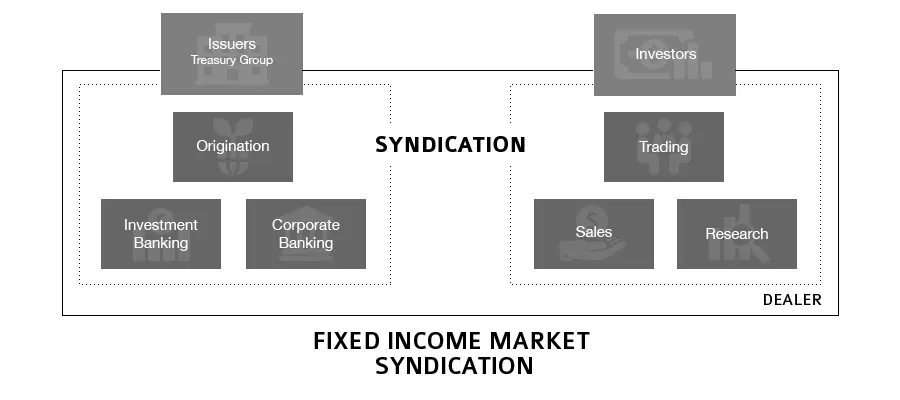

DEALER

Dealers in the Fixed Income Market

Dealers are financial institutions – predominantly subsidiaries of investment banks, commercial banks or investment companies – that play an important role by helping corporate and government entities make financial decisions and raise capital. Dealers provide advisory, underwriting and other services to bond issuers seeking to raise capital through bond financing.

Functions of dealers include:

- Financial services companies

- Bond origination – structuring, originating, underwriting and distributing new debt issues; legal documentation and credit rating advisory

- Corporate banking – diversified lending solutions for corporations and government entities

- Investment banking – financial advisory on capital raising and M&A transactions

- Sales, trading & research – execution and distribution of investment products; delivery of investment ideas and research products

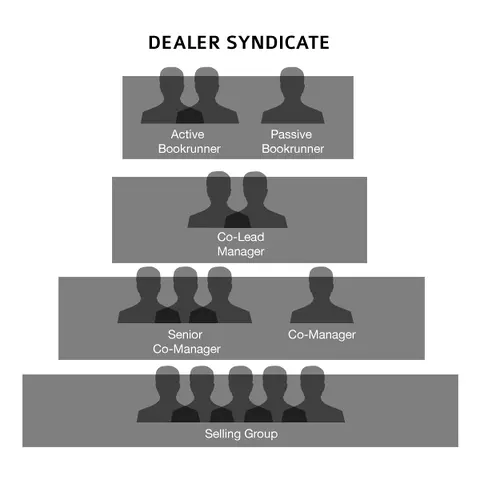

Syndicate of Dealers – Bond Underwriting Roles

New bond issues are underwritten by one or more lead managers and a syndicate of co-managers.

Standard roles within a syndicate are:

- Bookrunner – issuer-mandated dealer(s) responsible for the book building process. This includes marketing the issue, determining demand for the issue (i.e. engaging with investors), and pricing and allocating the issue. Bookrunners hold the largest responsibility in the syndicate.

- Lead manager – issuer-mandated lead manager(s) are responsible for the distribution of large portions of the new issue and support bookrunners through research. In large issues, multiple lead managers are appointed and they are known as co-lead managers. Though it is not required, bookrunners are typically also lead managers.

- Co-managers/Co-agents – dealers mandated by issuers or invited by the lead managers to participate in the new issue. Co-managers are brought into a deal for their relevant niche expertise, research abilities, and distribution networks.

Collectively, the syndicate will be compensated with an underwriting spread, which includes the management fee, the underwriter’s fee, and the selling concession. The underwriter’s fee is the cost of bringing the issue to market. After all expenses are paid, any remaining funds in the underwriter’s fee are distributed among the syndicate dealers.

Selling Group

Dealer syndicates may sometimes form a selling group to help market the new issue. This includes all financial institutions involved in the marketing or selling process that may or may not be in the dealer syndicate.

Active and Passive Dealer

A classification that has resurfaced in recent years is the active-passive classification for participants in the bond origination and underwriting process.

- Active dealers refer to dealers who are actively involved in the issuance process. This includes structuring, pricing, and allocating the new issue. Active dealers include lead managers and bookrunners. They typically receive a larger portion of the fees and are listed first in marketing material for the issue.

- Passive dealers refer to dealers who have a smaller role in the issuance process. This usually involves the research and distribution of the new issue. Passive dealers include co-managers and the selling group.