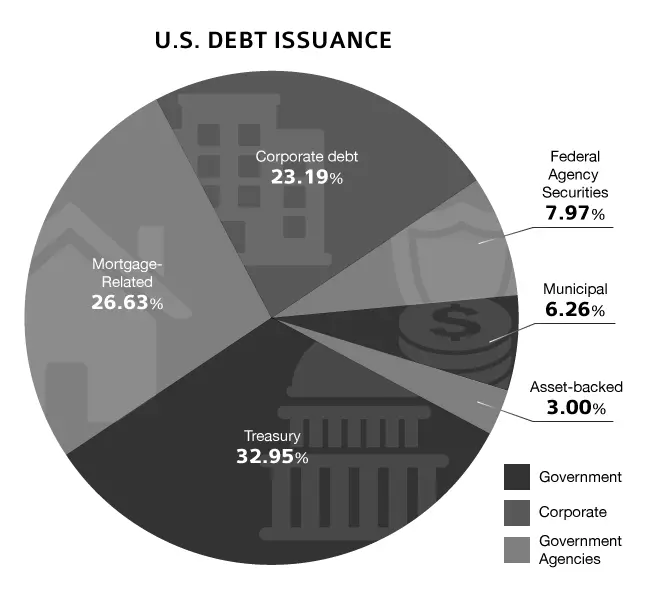

ISSUER

Issuers in the Fixed Income Market

Issuers raise funds by offering bonds and other debt instruments in the debt capital markets to fund existing operations or invest in new projects. There are two major types of issuers: governments and corporations. Depending on market conditions and issuer-specific financing needs, corporations will issue debt when it is favorable compared to equity-financing or other funding alternatives.

Corporations

Corporations utilize debt securities to raise capital and fund their capital expenditures. Holders of common stocks are “owners” who participate in the upside growth of the company. Holders of corporate bonds, on the other hand, do not share these profits – they can only expect interest payments and repayment of principal amount. Hence, the cost of debt is often “cheap” relative to equity. Further, in the event of issuer bankruptcy, bondholders must be fully repaid before common shareholders are paid. Therefore, fixed income securities such as bonds are often called “senior” securities. Main classes of corporate bond issuers include:

- Financial services companies

- Public utilities & energy-related companies

- Industrial corporations

- Diversified/conglomerates & telecom

- Real estate

Governments

Governments utilize debt securities to raise capital and plan capital expenditure because of its predictable cash flows and access to enormous capital sources.

- Federal/central government bonds often represent interest-rate benchmarks (risk-free rate) for major markets. Government bonds are generally highly liquid and are heavily regulated by central banks. Most major treasury bonds are issued through scheduled auctions with highly standardized processes. The U.S. treasury has the largest amount of outstanding bonds in the world and its bonds also have the most liquidity. U.S., Japan, United Kingdom, Germany, and Canada are some of the largest issuers of government bonds.

- Municipal securities – also known as “munis” – are issued by states, subdivisions of states such as cities, towns and other authorities to finance public-purpose projects such as road construction.

- Provincial government bonds are similar to municipal bonds with the exception that they are guaranteed by a provincial government as opposed to a municipality.

Government Agencies

Agency bonds are issued by two types of entities:

-

Government sponsored entities (GSEs) – privately-owned corporations

granted charter by the federal government that provide public

services. These entities are not direct obligations of the federal

government, but are implicitly backed by the federal government

because of the public service they provide. In some cases, federal

institutions have been established to explicitly connect GSEs to

the government. For example, housing GSEs are now under the

conservatorship of the Federal Housing Finance Agency and receive

funds directly from the U.S. Treasury to correct deficiencies in

their net worth. Examples of GSEs include:

- Federal National Mortgage Association (FNMA or “Fannie Mae”)

- Federal Home Loan Mortgage Corporation (FHLMC or “Freddie Mac”)

- Federal Home Loan Bank (FHLB)

- Federal Agricultural Mortgage Association (FAMA or “Farmer Mac”)

- Student Loan Marketing Association (SLMA)

-

Federal government agencies – divisions of the government that are

explicitly guaranteed by the full faith and credit of the federal

government. This means that the government is committed to pay

interest and principal back to investors at maturity. Examples of

federal government agencies include:

- Federal Housing Administration (FHA)

- Government National Mortgage Association (GNMA or “Ginnie Mae”)

Agency bonds issued by GSEs and federal government agencies are priced very similarly; however, due to the distinction that all federal government agencies are explicitly guaranteed by the federal government, GSE debt securities are priced at a slight premium. In general, all agency bonds are priced at a small premium to treasury bonds because of associated political risk – agency status could be modified or revoked – and because treasury bonds are the most liquid financial instruments in the capital markets.