The only explanation of the Canadian primary bond market you will ever need

Over the past decade, liquidity has decreased throughout the bond market. In the past, "if average market liquidity was a 5 on a scale of 1 to 10, today's markets might be something like a 3 or 3½," said Tony Rodriquez, co-head of fixed income at Nuveen Asset Management, in a 2014 interview with the Wall Street Journal. Liquidity has since continued on a downward trend as the difficulty of trading bonds increases. Electronic trading, on the other hand, is on the rise—evidence of a market that is increasingly interested in automation and digitization becoming integral parts of their workflows.

In a healthy and prosperous economy, a well-functioning and highly efficient primary bond market is a necessity, providing efficient allocations of capital to fund expansion and major investments. As it stands, though, the bond market is made up of many moving parts, all of which are in some senses competing, and in some senses working together, to create an agreeable outcome.

Current Status of the Canadian Fixed Income Market

To understand the way that digitization and financial technologies can affect change in the bond market, it is first necessary to understand the dynamics of the existing system .

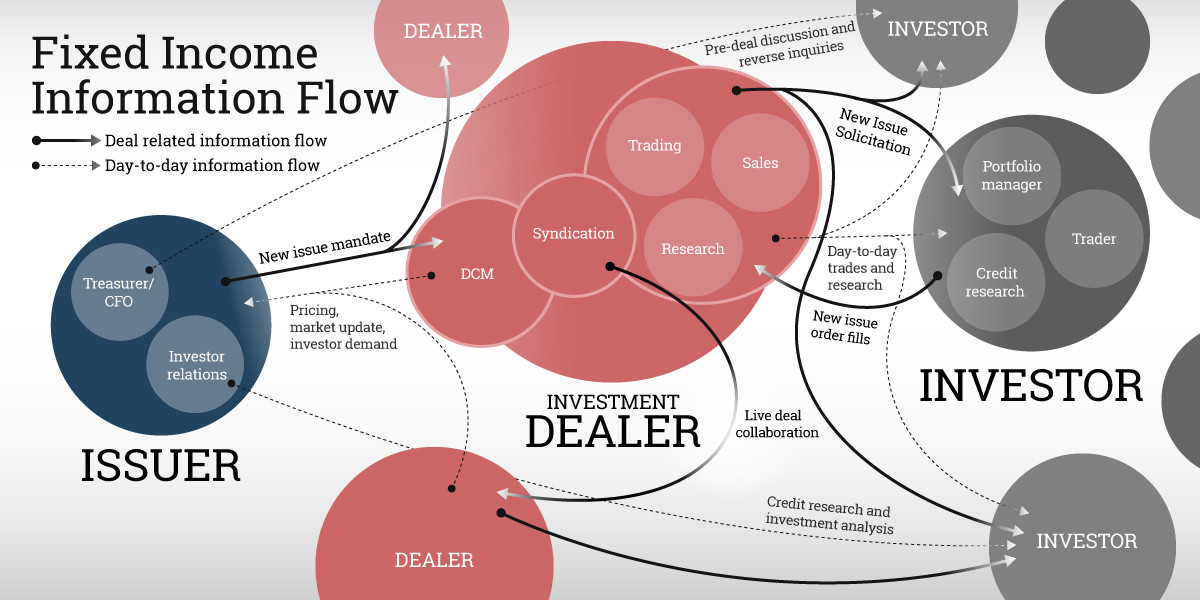

On one side, you have issuers who are looking to keep their cost of capital low, while also carefully managing risk—too high and the payout is not financially viable. A company looking to issue a sizeable bond—say, to finance a major acquisition, as Microsoft did when it bought LinkedIn in the summer of 2016 for $26.2B—will have a cadre of analysts and financial advisors monitoring the market to determine when it will be easiest, and cheapest, to issue debt.

Within a company looking to issue bonds , the treasury department’s major function is to maintain a healthy borrowing program, consisting of a strong investor base and an internal team who is well-informed about the capital market conditions. It is the job of the issuer to keep a watchful eye on the bond market in order to issue bonds while minimizing the cost and risks to achieve successful deal execution.

Also within an issuing company, the company CFO and treasurers take into account many economic signals, sector specific signals, their internal corporate finance criteria (such as debt to cash flow ratio, leverage, cash flow and credit ratings, just to name a few). These treasury teams also work with the debt capital markets (DCM) teams of several investment dealers, who provide professional services and client coverage. A big part of this coverage involves sending issuers information about pricing levels for new bond issues, timing to issue, and benchmarking with industry peers. Large corporations who issue bonds frequently typically also have an investor relations team to manage relationships with their major debt and equity investors.

On the other side of this equation, you have investors, typically institutional funds such as mutual funds and exchange-traded funds (ETF), pension funds, life insurance companies and hedge funds. Institutional funds are pooled funds which can range anywhere from $10M to over $100B.

Large funds will typically have a portfolio manager who oversees all investment decisions, a credit analyst who analyzes investment opportunities, some of which is provided by dealers, and a trader who strategizes and executes the buying and selling of securities. In most cases, only institutional investors have access to primary bond sales through their investment dealer. Many large funds have direct relationships with issuers as well.

An investor’s main objective is to find new deal opportunities in which to invest their funds, in order to meet the performance objectives of their fund. In the bond market, they are often institutionalized, and are seeking to maximize profit for their portfolio. Fixed income investors manage their assets by either trading bonds in the secondary market or purchasing new bond issues directly in the primary market.

Connecting the Two Sides

These two sides of the market require connectivity, however—this is where investment dealers factor into the market. The debt capital markets (DCM) teams are tasked with advising clients looking to raise capital on what type of debt will best meet their needs and on what terms. They are involved in every aspect of structuring and executing new debt issues – working with issuer clients to determine the right structure, working with legal counsels to document the deal, and working with internal teams including syndication, sales and trading desks to price and distribute it. Their main objective in the market is to connect issuers and investors, and to execute large and often complex transactions smoothly and efficiently.

They play the role of expectation manager, as well, through their role in communicating information between the two stakeholders in a fixed income deal. To do this, DCM teams maintain relationships with issuer clients by providing market research and data constantly so that they are in a position in order to execute new issue transactions successfully.

The major dealers in Canada are the big 6 banks , whose DCM teams are around 30 - 60 people. There is fierce competition between the banks to act as the bookrunner or lead for a new bond issue, and in order to maximize their commission they must ensure that best practices are followed. Typically bookrunner commissions range between 0.3% - 1.5% of the total deal (i.e. for a $1 billion deal, commission will range from $3M - $15M). Within an investment dealer, DCM teams work with the Syndication team, who provide a channel to Sales, Trading and Research departments.

The majority of new bond issues in Canada are syndicated , which allows dealers to spread risk and take part in financial opportunities that may be too large for their individual capital base. Investment dealers within a syndicate group will typically split the fee based on an issuer’s discretion.

Through dealers, issuers are able to finance large scale projects by accessing investors, but each lacks full insight into the motivations and incentives of the other.

To learn more about how machine learning technologies can increase liquidity in primary bond markets, click here .

About Vuk Magdelinic:

Before founding Overbond, Vuk’s career spans over 10 years in capital markets and technology. As PwC Risk and Regulatory consulting manager Vuk led large digital transformation programs at Deutsche Bank and BNY Mellon in New York City. Prior to that he worked at CIBC Fixed Income trading floor in Toronto in structured products origination capacity. Vuk has collaborated on numerous publications addressing key trends in fintech innovation. Vuk holds electrical engineering degree from University of Toronto, MBA from Ivey School of Business and is an avid abstract painter.