Case Study: How Interoperability Brings Automation to Bond Trading

FIX API Interoperability: Bringing Automated Trading To Complex Dealer Desk Technology

Why is trading technology interoperability so important?

Overbond COBI-Pricing LIVE gives desks the ability to fully automate 30 percent of their RFQs and execute an additional 20 percent with trader supervision. This is possible because of three factors: AI models such as COBI-Pricing LIVE that can price fixed income securities and score their liquidity; speed from cloud computing; and protocols that allow for data aggregation and increased interoperability of the systems used in trading workflows.

Interoperability is the ability of different systems or programs to communicate with each other, exchange information, and use that information. It is particularly important for bringing automated trading to the sell-side and buy-side desks because these desks traditionally have five to 10 pre-existing systems necessary to conduct trading. Automating trading workflow is possible because COBI-Pricing Live is fully interoperable with the existing technologies on the desk.

Overbond’s COBI-Pricing LIVE uses three layers of interoperability to automate trading: it ingests and aggregates data from multiple sources, it integrates with the legacy systems on the desk, and it communicates with electronic trading venues.

COBI-Pricing LIVE aggregates data from multiple sources including vendor feeds, internal historical records and settlement-layer volume information for OTC trades from providers such as Euroclear. To ingest data from these diverse sources requires interoperability between COBI-Pricing LIVE and the systems that provide the data.

Interoperability of COBI-Pricing LIVE with legacy internal systems means trading desks can make COBI-Pricing LIVE their own by accessing recorded transaction history to train the model according to the trading style of the desk and significantly increase P&L.

Interoperability with electronic trading venues allows for the ability to trade on multiple platforms and opens the door for smart order routing , allowing desks to optimize execution.

COBI-Pricing LIVE interoperability

COBI-Pricing LIVE now offers protocol and system agnostic integration with venues and e-trading systems used by sell-side and buy-side trading desks through RA Platform 3.0, an open API enterprise software platform from Rapid Addition, a provider of electronic trading middleware.

Rapid Addition’s expertise in FIX protocol, counterparty, and market-place connectivity via its open API enterprise software platform will allow global fixed income trading desks to seamlessly integrate AI-driven bond pricing and liquidity scoring analytics into their workflow, regardless of which internal OMS, e-trading system, direct venue connectivity, cloud or on-premise solution they currently use. These API connections allow for internal system integration, pre-and post-trade external data vendor ingestion, and liquidity venue connectivity — ultimately creating a streamlined system capable of automating RFQ flow using Overbond’s AI engine.

Interoperability allows COBI-Pricing LIVE to aggregate data from multiple sources including vendor feeds, internal historical records and settlement-layer volume information for OTC trades from Euroclear.

Interoperability with legacy internal systems means trading desks can make COBI-Pricing LIVE their own by accessing recorded transaction history to train the model according to the trading style of the desk and significantly increase P&L.

Interoperability with electronic trading venues gives desks the ability to trade on multiple platforms and opens the door for smart order routing, allowing desks to optimize execution.

Overview of the Current Process

Technology has been enabling automation in equities for two decades. It’s now poised to enhance the bond market. Increases in fixed income electronic trading volumes have driven enhancements in trading desk operations over the previous five years, making the lives of traders easier in today’s natively digital world. This is now possible because of three factors: AI models such as COBI-Pricing LIVE that can price fixed income securities and score their liquidity; speed from cloud computing; and protocols that allow for data aggregation and increased interoperability of the systems used in trading workflows.

- Real-Time Pricing of Securities

- The fixed income industry was focused on end-to-end trade workflow automation and real-time pricing of bond securities

- AI algorithms were designed and configured to assist traders with aggregating data sources and automating pricing

- Interoperability allows end-to-end automation by facilitating the aggregation of data from multiple sources, the integration of Ai and connectivity with multiple trading venues

- Overbond’s AI algorithms

- Interoperability with multiple venues allows Overbond’s AI algorithms to examine which venue trades should be routed to for execution based on past performance and real-time market conditions

- Best execution is determined by price and liquidity factors across multiple data sources

- Interoperability will expand the use of algorithms in fixed income trading and create more growth and automation as new execution pathways and scenarios continue to get discovered with AI

- RapidAddition (RA) interoperability

- RA facilitates interoperability with venue connectivity, the RFQ automation engine, and any other OMS or customer system integration to support implementation of Overbond analytics

Challenges With Legacy Systems And Processes

When the RFQ is received by the trader via the Bloomberg (or other) terminal or a phone call, there could be several different methods of pricing the bond, below is an example of some of these options:

- CBBT price taken from Bloomberg covering most of the cases

- Fixed Yield quoted – for the special type of the security

- Price Range quoted – a certain range is added

- A certain spread range set – this might be quite wide

The decision on which of these methods should be used, or whether the CBBT (Bloomberg composite feed) price is good would have to be taken by the trader on a case-by-case basis. A loss of RFQ (as a sell-side market maker) may occur due to the manual and time-consuming nature of checking fixed yields and certain spread ranges. Comparing the bond that is mentioned in the RFQ, with a similar bond from a peer, would provide good insight into the likely price of the bond, however, this would also take time.

Trader Workflow Objectives And Constraints:

- The time window within which the trader is supposed to respond to an RFQ is 1 to 3 minutes; however, 1 to 2 minutes is considered ideal.

- The current cover (difference between accepted trade price and next best quote) is 5 to 10 cents.

- Trader must deal with approximately 300 to 700 RFQ’s per day

- On average, around 30%- 40% of RFQs are responded to with a hit rate of 10%– 12%

Drivers of the problem

The primary problem that the trader faces is due to the low confidence in prices suggested by Bloomberg CBBT and third-party applications that are currently used:

- Bloomberg CBBT

- Current third-party pricing provider

The price suggested by Bloomberg CBBT is a composite price based on the most relevant executable quotations on Bloomberg’s Fixed Income Trading platform. The composite is based on current market activity for that bond. If the bond is illiquid, for whatsoever reason, the CBBT price would not represent the true price. This is especially the case when dealing with high yield bonds or bonds with varying liquidity profiles.

The pricing methodology is based on a certain pre-defined methodology. The trader’s confidence in this system is low as the pricing methodology is not dynamic and this leads to the suggested pricing is incorrect. As perceived by the trader, there is a large difference in cover (the difference between accepted price and next best available quote) when the deal is won (5-10 cents)

These factors lead to low confidence in the suggested prices and traders must constantly spend a great deal of time and effort in manually adjusting prices based on prior knowledge and intuition. The major trade-off is thus accuracy versus time, leading to missed deals and direct downward pressure on desk P&L. Clients value speed of execution. Interoperability between data feeds, internal systems and trading venues speeds the RFQ process by facilitating automated trading in near real-time.

Challenges With Data Aggregation

One of the first hurdles facing fixed income pricing AI is the lack of a centralized source of trade data. Data feeds from any single electronic provider don’t provide enough information for calculating prices and liquidity scores for illiquid securities. This problem is solved by aggregating data from multiple sources including vendor feeds, internal historical records and settlement-layer volume information for OTC trades from providers such as Euroclear. This data aggregation layer requires interoperability between multiple data feeds and real-time AI data mapping.

Data Intake & Pre-processing

The Overbond platform sources raw trading live date and fundamental data via Refinitiv’s live platforms. Our data sources include Refinitiv, S&P Global Market Intelligence (company level fundamental data) as well as various other sources. Overbond sources primary dealer quotations from a community of large IG issuers and investor preferences through direct feedback loops.

This raw data is then structured in the Overbond databases. Trading data and fundamental data are structured and mapped to the appropriate issuer ID. The data is systematically scrubbed for anomalies and null values. Finally, a set of key input factors are generated based on the raw input. These include but are not limited to factors that measure secondary market spread movements, recent issuance pricing levels, nearest neighbor credit ratings, and fundamental financial metrics. These factors are divided between sector and company-specific and are used as inputs to the machine learning models.

Model Training

The subsequent stage for the machine learning algorithm is to train and apply several models to calculate the output pricing levels. An Ensemble Learning strategy is used in three phases, meaning multiple models are combined to elevate overall robustness at each training stage. These models are each trained using a subset of the past data, ranging from one day, one month to a maximum of ten years. Advanced sampling techniques were used to account for data gaps for illiquid issuers in order to construct yield curves for all tenors and all issuers in coverage universe.

COBI-Pricing Data Intake

Successful data pre-processing is the key stage and pre-requisite for the COBI-Pricing algorithm operation. The precision of the algorithm output is critically dependent on the accuracy, timeliness, and relevance of the pre-processed input data. Overbond sources raw data from major data suppliers in the financial sector, including Refinitiv, Ice, The Six Group, EDI, MarketAxess, Tradeweb, Euroclear, Clearstream, DTCC, CDS, S&P Global Market Intelligence, major credit rating agencies, as well as other sources. The data COBI-Pricing algorithms use includes the following:

| Pre-processed Data | Source | Update Frequency | Relevance |

|---|---|---|---|

| Secondary market transactions data | Refinitiv, Ice, The Six Group, EDI, MarketAxess, Tradeweb | Intraday | Live prices and yields of companies’ bonds are used to measure spread movements in the coverage universe. |

| Settlement layer data per ISIN liquidity profile | Euroclear, Clearstream, DTCC, CDS | Intraday, end of day and historical | Settlement layer data when adjusted and merged with correct trading time stamp can augment the view into true liquidity of the particular ISIN as it contains settled trades by counterparties that were executed on the OTC level and otherwise do not appear in other consolidated data feeds. |

| Nearest Neighbour Credit per Rating and Industry Sector | Refinitiv, Ice, The Six Group, EDI, MarketAxess, Tradeweb, DBRS, Moody’s, Fitch, S&P | Weekly updates, quarterly filing cadence | Issuer’s industry sector cluster and past bond issuances and their ratings as well as composite rating for the issuer overall indicate the company’s risk level and benchmarking category. They are used to train the models and to back-test the accuracy of COBI-Pricing output. |

| Fundamental Financial Metrics | S&P Global Market Intelligence | Weekly updates, quarterly filing cadence | The company’s fundamental financial data is an indicator of the company’s credit-worthiness, and by extension, their cost of borrowing across tenors reflected in the bond pricing. In addition, fundamental metrics indicate the liquidity need of the company and its short term need to raise financing as well as leverage ratios. The financial profile of a company aids with clustering analysis of companies with similar characteristics. |

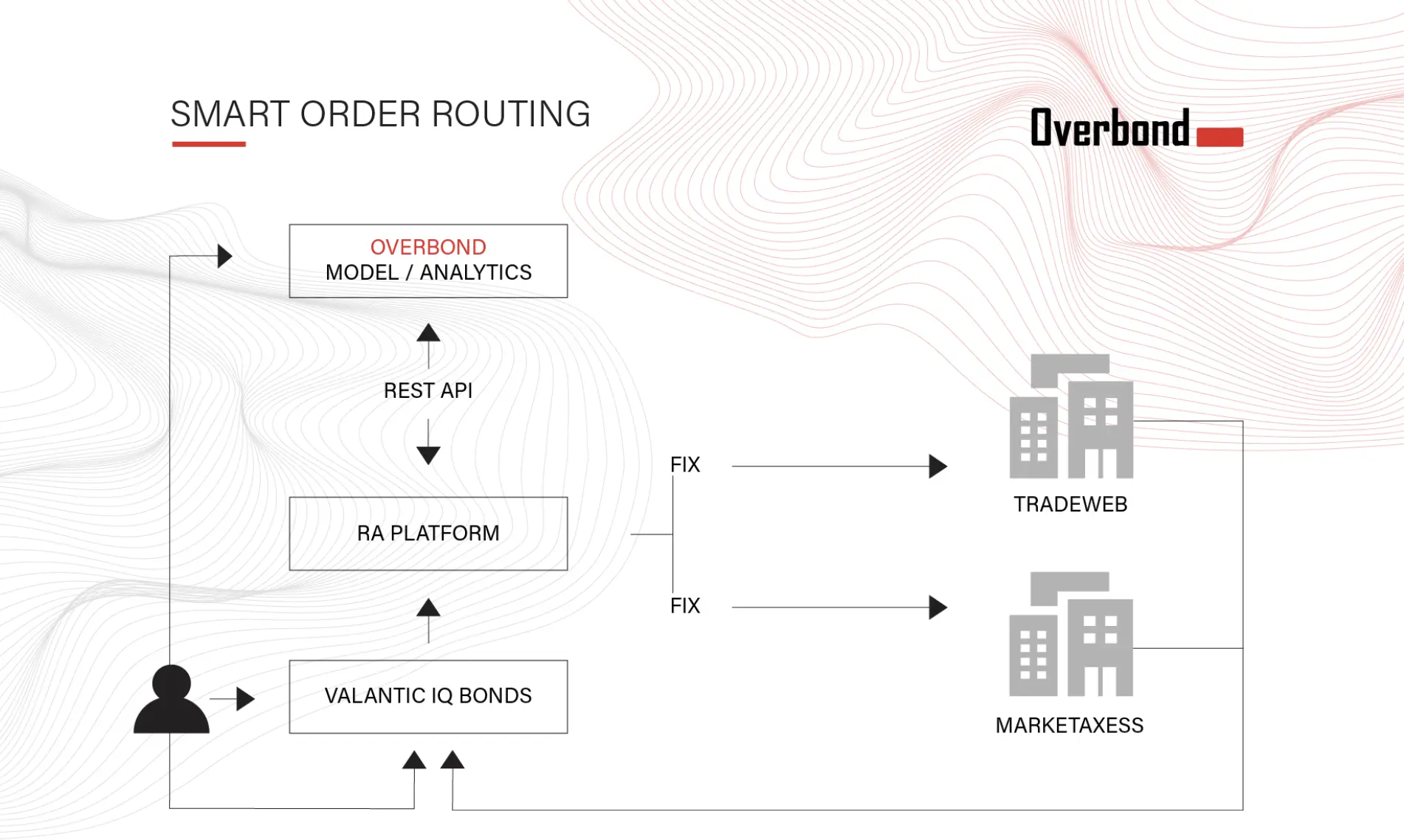

Case A - EUR sell-side credit trading desk

The diagram below and the following paragraphs provide a description of how GBP sell-side credit trading desks use internally built OMS systems and can connect with Overbond & RA interoperability layer to achieve best execution:

Smart Order Routing for Best Ex

Overbond and RapidAddition(RA) deliver interoperability and direct venue connectivity for bond trading automation services.

- Electronic bond trading using Valantic IQ e-trading platform

- Dealer data aggregation across multiple venues, across all currency’s markets are made, using sell-side desks recorded transactions history

- Overbond AI Modelling engine with RA interoperability layer for Smart Order Routing

- Trade routing for Best Ex to venues Tradeweb & MarketAxess

- External data vendor connectivity (pre-and post-trade) and direct venue connectivity

Interoperability ties all parts of the RFQ and smart order routing together. It allows data aggregation, the integration of AI modelling and external pre-and post trade vendor connectivity.

Overbond Model / Analytics Layer

API connections ensure sell-side dealers have a fully integrated (frontto-back) system capable of automating RFQ flow in any currency they make markets in, internal system connectivity with their recorded transactions history, external data vendor connectivity (pre-and post-trade) and direct venue connectivity

Case B - GBP Dealing sell-side credit trading desk

The diagram below and the following paragraphs provide a description of how GBP sell-side credit trading desks use internally built OMS systems and can connect with Overbond & RA interoperability layer to achieve best execution:

Trade Routing for the Sell-Side

Sell-side dealers are increasingly relying on AI applications to price bonds in live trading. This includes the consumption of increasing amounts of alternative data and using new methods of fixed income pricing analysis.

Overbond & RA’s interoperability layer provides access to MTF’s, connected via APIs on FIX protocol, allowing sellside dealer clients to implement Overbond AI models.

Rapid Addition

RA interoperability middleware will provide venue connectivity, RFQ engine, and any other OMS or customer system integration to support implementation of the Overbond analytics.

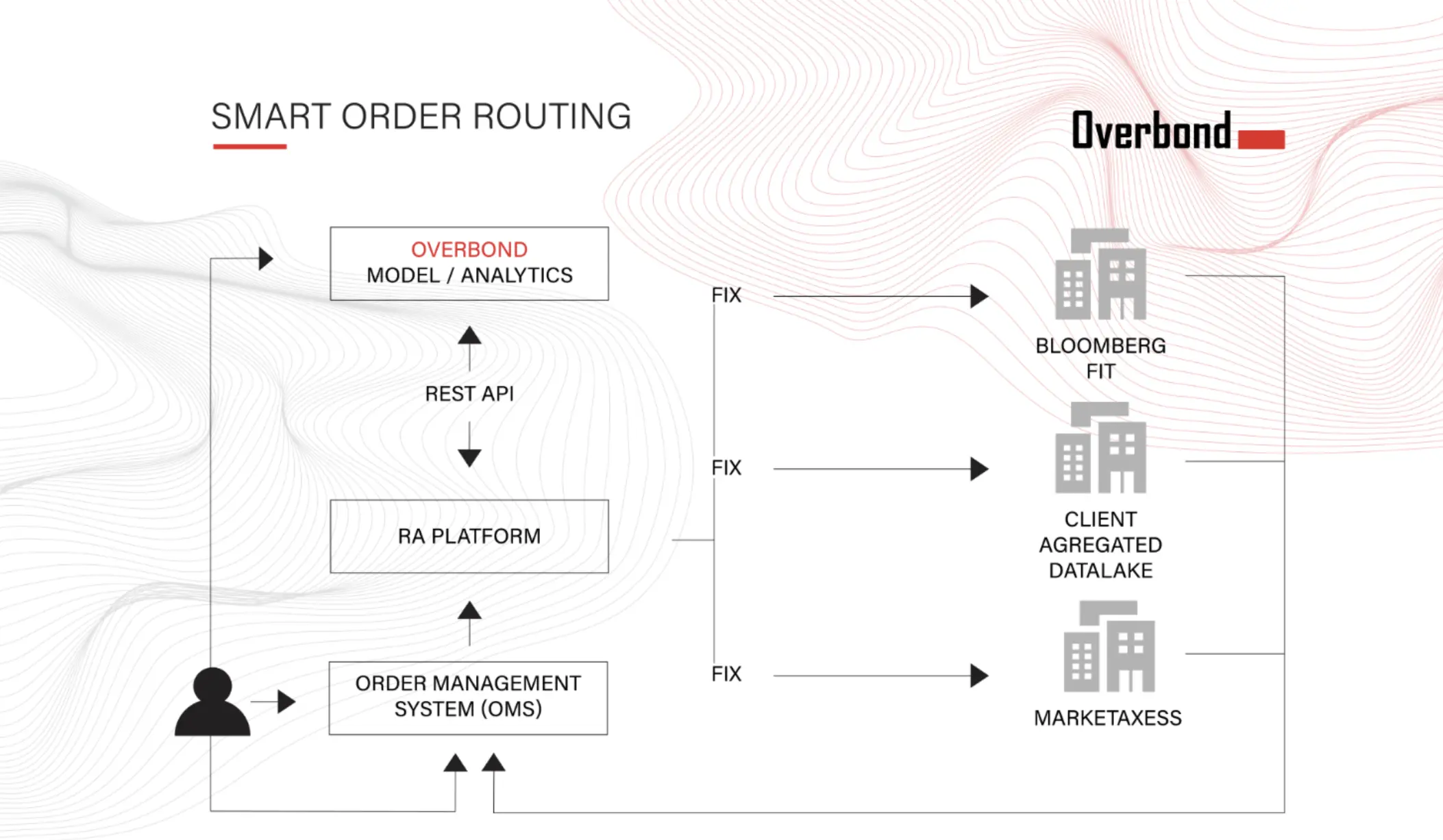

Case C – USD Buy-side credit trading execution desk

The diagram below and the following paragraphs provide a description of the desk technology interoperability with client-side built data lake (client aggregated data lake) along side custom built OMS system.

Smart Order Routing for Best Ex

Overbond and RapidAddition(RA) deliver interoperability and direct venue connectivity for best execution and bond trading automation services.

- Dealer data aggregation across multiple venues, across all currency’s markets are made, using client aggregated data lake and recorded OMS transactions history

- Overbond AI Modelling engine with RA interoperability layer for Smart Order Routing

- Trade routing for Best Ex to venues Tradeweb & MarketAxess

- External data vendor connectivity (pre-and post-trade) and direct venue connectivity

Client Aggregated Data Lake

With buy-side increasingly relying on AI applications to aggregate data and price fixed-income securities in live trading, Overbond fills the gap by providing LIVE data aggregation and real-time analytics for the fixed-income market best execution.

Business Impact

Interoperability with electronic trading venues not only allows for the ability to trade on multiple platforms but also opens the door for smart order routing, allowing desks to optimize execution. Using Overbond’s COBI-Pricing LIVE gives desks the ability to fully automate 30 percent of their RFQs and execute an additional 20 percent with trader supervision. The precision of AI, the speed of cloud computing and the interoperability with trading desk systems are making automated trading a reality.

Specific use cases for the COBI-Pricing algorithm application are examined to identify business objectives and key benefits below. Overbond client organizations include sell-side institutions with significant trading volumes (200-2000 RFQs+ a day per trader). Their innovation groups actively explore new technologies that can serve as the catalyst for trading automation and improved risk management, trade flow, pre-trade and post-trade analytics.

| AI Application | Business Objectives | Key Benefits |

|---|---|---|

| Intelligent automation and enhanced decisionmaking |

|

Overbond COBI- Pricing AI models aggregate historical data from multiple sources and optimize pricing for bonds with varying liquidity profiles. Overbond COBI Pricing can enhance users’ bond trading workflow by providing precise executable prices in up to 30% more situations when there is no directly observable trading price in the market. Bond trading execution desk revenue can be grown significantly through their access to this insight. COBI-Pricing enables fully automated bond trading workflow with various curve visualizations and front-end trade analytics tools that are natively integrated with trader’s desktop. As a dealer, boost your RFQ hit ratio with pricing feed with margin optimization model add-on, discover deep bond liquidity profile, and predict investor behaviour with buy/sell indicators Sell-side credit and rates trades can grow their RFQ response volumes significantly with precision and confidence, growing accordingly desk P&L. |

Implementation Considerations

Institutions considering AI predictive analytics implementation and big-data transformation projects can employ acceleration utilizing externally calibrated models and market signals. Below are several key considerations and questions for executives in charge of AI roadmap:

- What is the current state of our fixed-income in-house data?

- What are our data science and engineering capabilities?

- Are we building AI capabilities to grow revenue or cut cost?

- How can we redefine the boundaries of our data universe or identify alternative data sources necessary to feed AI engine?

- Given that AI learning curve is steep where do we begin?

- How do we create and execute AI proof of concept use cases rapidly?

- What are key success factors for our AI roadmap?

Custom AI Services

Overbond works with clients to identify and recommend practical AI analytics

use cases that are aligned with strategic goals of the financial institution. We

help assess current-state AI capabilities, and define roadmap to help clients

realise value from AI applications. We manage cross-channel data flows

across multiple systems and enable custom font-end visualizations.

Proven Methodology

With our targeted approach and implementation methodology, we quickly

demonstrate value of AI analytics to test use cases, enabling client-side

change management approach and stakeholder buy-in.

Operational Acceleration

We help clients build and deploy custom AI solutions to deliver proprietary

analytics and tangible business outcomes. Our experience combines

calibrated models, design patterns, engineering and data science best

practices, that accelerate value and reduce implementation risk.

AI Analytics As-a-Service

Overbond helps customers design and oversee mechanisms to optimize and

improve existing fixed income credit valuation, issuance and pricing

prediction and pre-trade opportunity monitoring using AI. Our team of worldclass data scientists and engineers manage an iterative implementation

approach from current state assessment to operational handover.

About Overbond

Overbond specializes in custom AI analytics development for clients implementing trade automation workflows, risk management, portfolio modeling and quantitative finance applications. Overbond supports financial institutions in the AI model development, implementation and validation stages as well as ongoing maintenance.

Contact:

Vuk Magdelinic

Chief Executive Officer

+1 (416) 559-7101

vuk.magdelinic@overbond.com