BOND PRICES

Breaking down Bond Cash Flow

When bond issuers sell bonds to finance new projects, maintain ongoing operations, or refinance existing debts, they enter a contractual agreement to make coupon payments on the coupon payment dates and to repay the principal amount on the maturity date. In the primary bond market, the issue price is typically set at or near par, which is usually either $1,000 or $10,000 face value. The price of a bond fluctuates over time depending on prevailing market conditions or company-specific factors, which are reflected by underlying interest rates and credit spreads.

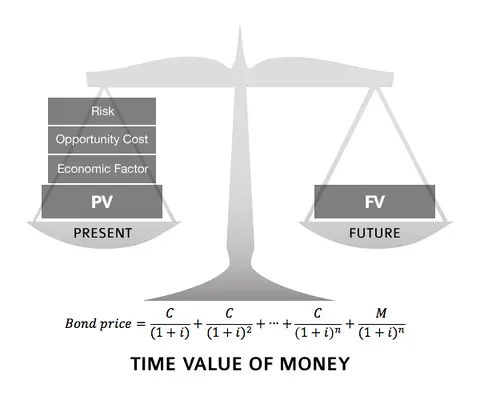

Time Value of Money

A central concept in bond pricing is the time value of money. It is the idea that money available today is worth more than the same amount in the future. For example, $1,000 is worth more today than a $1,000 in a year’s time because of economic factors (e.g. inflation), opportunity cost (e.g. yield from other investment opportunities), and risk (e.g. the bond issuer could default before one year) associated with future cash flow. As a result, future cash flows cannot be priced the same as cash in the present. These future cash flows must be “discounted” to adjust for the passage of time. A payment that is further out in the future will result in a larger discount factor and lower present value to reflect the time value of money.

Bond Price

A bond’s price is determined by summing up future cash flows discounted to the present value:

C = coupon payment

n = number of payment periods

i = required yield for each payment period

M = principal amount

Required Yield

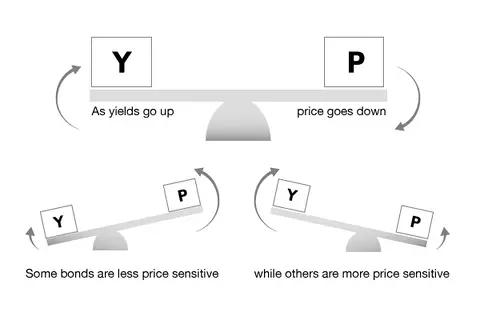

Required yield is the discount rate used to convert future cash flows to present values to derive the price of a bond. The required yield, also known as the bond yield, is comprised of the issuer’s market issuance premium – the “credit spread” – and the risk-free rate (e.g. U.S. treasury yield). Bond yield has an inverse relationship with bond price. As yield or required return increases, the bond price decreases in order to make the offering more appealing for investors. Conversely, if bond yield decreases, bond price will increase.

Sample Corporate Bond New Issue Pricing

| Benchmark U.S. Treasury Bond | UST 1.625% due 5/16/2026 | |

|---|---|---|

| Benchmark Yield | 1.566% | Risk-Free Rate |

| Spread to UST Curve | 50 bps | Credit Spread |

| Re-Offered Yield | 2.066% | Bond Yield |

Risk-Free Rate

The risk-free rate is a benchmark rate that represents a similarly termed risk-free investment. This component of yield accounts for the return an investor would require to forgo an alternative risk-free opportunity. These benchmarks are typically government issued bonds that have low risk of defaulting (e.g. U.S. treasury, Government of Canada). Major factors affecting the risk-free rate include:

- Policy - changes to government monetary and fiscal policies will cause government bond yields to fluctuate.

- Supply and demand – the laws of supply and demand will push government bond yields to a market equilibrium.

- Inflation outlook – inflation outlook reflects the buying power of the economy. As a result, higher inflation should drive the government bond yields up because investors will require higher cash flow to compensate for the decrease in buying power.

Credit Spread

The credit spread is the additional return an investor would require to invest in a non-risk free bond offering. It is measured in bps (1 bp = 0.01%). Credit spread is determined by the issuer’s credit strength, comparable issuers in the market, and underlying market conditions. It should be noted that the credit spread has an inverse relationship with market conditions. In bearish market conditions, the credit spread will increase (widen), while the credit spread will decrease (tighten) in bullish market conditions. Major factors affecting the credit spread include:

- Market conditions – investors will require higher returns to compensate the increased risk of investing in poor market conditions, resulting in a wider credit spread.

- Company financial strength – declining financial health will make an issuer’s bonds riskier (default/credit risk), causing the credit spread to widen to reflect this increased risk.

- Company outlook – corporate events (e.g. mergers, bankruptcy, earnings call) can reveal new information in the market that will be reflected in the credit spread. A negative corporate event will cause the credit spread to widen.

Premium, Par, and Discount

As demonstrated in the formula above, a bond’s price is directly linked to coupon rate and the yield. If the coupon rate is higher than the yield, the bond price will be greater than par. This is known as a premium bond. Investors pay a premium for these bonds because the coupon and principal payments are higher than fair or required returns in the market. Conversely, if the coupon rate is lower than the yield, the bond price will be less than par. This is known as a discount bond. Investors demand these bonds at a discount price because the coupon and principal payments are less attractive than similar market opportunities.

Illustration – Bond Price and Yield

This graph illustrates the relationship between an 8% coupon with 4% yield (premium bond), 8% yield (par bond), and 12% yield (discount bond). As the time to maturity approaches zero, all three bonds converge on the par price.

'Clean' and 'Dirty' Price

Bonds accrue interest in between coupon payments. A bond’s clean price is the price that excludes the interest accrued after the most recent coupon payment. A bond’s dirty price includes the additional interest accrued after the most recent coupon payment.

Accrued Interest

A bond’s coupon payments compensate investors for the risk and opportunity cost of loaning money to the issuer. As each day passes, the bond is accruing interest. This interest is “earned” by the investor daily and is paid out periodically in discrete installments as coupon payments. Generally, the interest accrued between two coupon periods can be calculated by:

It is important to note that different markets have different counting conventions.

Bond Sensitivity

Bond price and yield have an inverse relationship. When yields are low, bond prices are high, and when yields are high, bond prices are low. In addition, the longer the maturity the more the bond’s price is affected by yield. This relationship is the bond price’s sensitivity to yield. The precise degree of this relationship can be quantified using the concept of (Macaulay) duration.

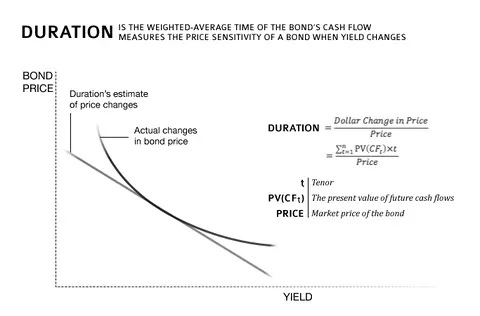

Duration

There are two interpretations of duration:

- Duration is the weighted-average time of the bond’s cash flow

- Duration measures the price sensitivity of a bond when yield changes – measures the approximate percentage change of price with each percentage (100 bps) change in yield

Duration can be calculated by:

The duration formula assigns a weight to each future cash flow depending on the distance of time from the present (e.g. higher weighting further from the present). The sum of these weighted cash flows divided by the market price of the bond provides a linear approximation of the bond price’s proportional change to yield.

Modified Duration

Modified duration is an extension of Macaulay duration, accounting for interest rate movement to provide a more accurate measure of price sensitivity. It can be calculated by:

As a result, the sensitivity in price can be denoted by:

For a bond with a modified duration of 4, a 1% change in yield will result in an approximate 4% change in the bond price.

A Note on Negative Yield

In an attempt to stimulate the economy, many central banks and governments reduced policy rates (government and central bank yields) and introduced stimulus bond buying programs, leading to flatter yield curves or even negative-yielding 10-year government benchmark bonds (investors are paying to lend their capital). Issuers and investors need to be considerate of this phenomenon. Click here to read more about this issue.

THE IMPORTANCE OF DURATION MANAGEMENT

Duration Management

Almost all bond market participants are embracing the record low interest rate environment nowadays. However, investors should be especially alert to their bond holdings’ high vulnerability to potential rising rates not only because the low yields provide almost no buffer to bond price decrease but also because the average duration of bonds has gone up as corporates and governments tend to issue longer bonds. Thus, duration management becomes increasingly important in mitigating interest rate risk.

Key Duration Concepts

- Duration measures the degree of bond price movement in response to change of interest rate

- Lower Coupon Rate results in a Higher Duration

- Longer Term results in a Higher Duration

- Higher Duration means Higher Price sensitivities to a chance in interest rate

As discussed earlier, duration measures the degree of bond price movement in response to change of interest rate. Although it is the most commonly used interest risk management tool by investors, it is crucial to understand that interest rate risk exposure cannot be completely eliminated due to its uncertainty nature. With this understanding, let us look at how interest rate risk can be managed with duration management:

- The most popular approach is to adjust the weighted average maturity of the portfolio. Increasing the weight of bonds with shorter maturities will reduce duration. Conversely, duration can be increased with the purchase of longer bonds.

- All else being equal, fixed rate bonds have a higher duration than floating rate bonds. Therefore, investors can trade fixed bonds for floating bonds to reduce duration.

- Higher coupon bonds have a shorter duration than lower coupon bonds with similar maturity because of higher cash flows. In other words, the price impact of interest rate risk is relatively reduced due to a higher credit risk component in the portfolio.

It is also important to note that the lower the coupon rate, the higher the convexity of a bond, a measure of non-linear relationship of bond prices to changes in interest rate.

Key Bond Concepts

Duration Risk: Duration is a measure of sensitivity of the price - the value of principal - of a fixed-income investment to a change in interest rates. Duration is expressed as a number of years. Bond prices are said to have an inverse relationship with interest rates.