STANDARD COVENANTS

What are Covenants?

The issuer and a trustee enter into a legally binding agreement called a trust indenture. The indenture outlines all financial covenants, the terms of agreement (covenants) that protect all parties’ interests until the maturity of the bond or the specified duration of the covenant. Violation of covenants will put the issuer in technical default, triggering remedies that protect investor interests (e.g. foreclosure, increased coupon rate). Issuers should be cautious when stipulating covenants, as they may hinder their ability to effectively utilize proceeds of the new issue and restrict business operations.

Negative Covenants

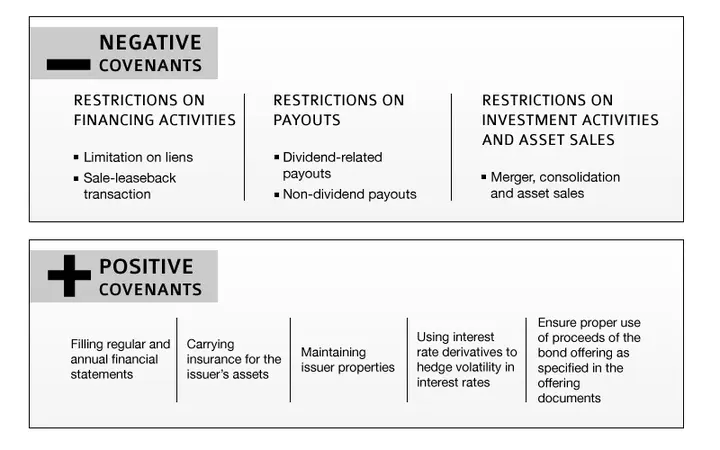

Negative or restrictive covenants limit certain issuer activities. Negative covenants may restrict financing activities, payouts, investment activities and asset sales. Negative covenants include:

-

Restrictions on financing activities – covenants that limit

further issuance of debt and sale-leaseback transactions.

Restrictions on financing mitigate risk of claim dilution,

by limiting additional debt that may increase default risk

and reduce recovery amount.

- Limitation on liens restricts an issuer from using company assets to secure future debt. This protects the bond’s priority in the capital structure. Key considerations include which assets this covenant applies to and which assets would be exempt.

- A sale-leaseback transaction is a method of raising short-term capital whereby the issuer sells specific assets to another entity and agrees to lease the assets back for a fixed term and rate. Sale-leaseback agreements are a liability that holds higher priority claim than bondholders, so covenants are in place to limit these actions.

-

Restrictions on payouts – covenants that restrict the amount

of payouts. These covenants protect bondholders from the issuers

paying out proceeds from liquidating firms assets

to other stakeholders (e.g. shareholders). There are two groups

of payout covenants:

- Dividend-related payouts – limits the amount of dividends the issuer may distribute to its shareholders.

- Non-dividend payouts – limits payouts other than dividends. This group includes restrictions on share repurchases and redemption of subordinated debt.

-

Restrictions on investment activities and asset sales – covenants

that protect bondholders from risky issuer investments and major

corporate events (e.g. mergers).

- Merger, consolidation, and sale of assets covenants prevent an issuer from merging with another entity or selling off significant portions of their assets without limitations on use of proceeds (e.g. reinvest in the business or redeem outstanding debt).

Positive Covenants

Positive, or affirmative, covenants require issuers to remain in compliance with the agreement by meeting specific requirements and completing certain actions. These covenants include carrying insurance policies, maintaining certain performance standards, and providing financial statements. Positive or affirmative covenants include:

- Filing regular quarterly and annual financial statements

- Maintaining issuer properties

- Carrying insurance for the issuer’s assets

- Using interest rate derivatives to hedge volatility in interest rates

- Ensure proper use of proceeds of the bond offering as specified in the offering documents

Financial Covenants

Financial covenants require issuers to maintain certain financial ratios. They are performance metrics covenants that provide remedies if the issuer’s financial health deteriorates. There are two types of financial covenants:

- Incurrence test – an action-triggered covenant that becomes effective if the issuer incurs additional debt or makes restricted payments to the detriment of bondholders. The incurrence test references a key financial ratio (e.g. interest coverage ratio, leverage ratio) and is triggered if an incurrence action violates the condition of the test (e.g. incur additional debt exceeding the leverage ratio limit).

- Maintenance test – issuer is required to maintain certain financial metric limits. Violating these maintenance tests will automatically put the issuer into technical default.

Financial covenants may include:

- Net worth – excess of issuer’s assets over liabilities. This covenant prevents issuers from paying large dividends to shareholders that would reduce net worth below the set limit.

- Debt-to-EBITDA/leverage ratio – ensure that the issuer has sufficient earnings to support debts.

- Interest coverage – ensure that the issuer has sufficient earnings to pay interest on outstanding debts.

- Fixed charges coverage ratio – ensure that the issuer has sufficient earnings to cover all non-operating cash needs.

- Debt-to-EBITDA ratio – measure the issuer’s ability to pay off debt obligations.

Other Covenants

Other common covenants include:

- Events of default – these covenants are a list of default conditions under which the issuer violates its terms of agreement. This can include bankruptcy, subsidiaries of the issuer not paying principal or interest as scheduled, not filing financial statements on time, or a legal judgment in excess of a certain amount. There is usually a grace period (30 to 90 days) to cure these covenants before the bonds become immediately due.

- Change of control (CoC) provision – a CoC covenant allows investors to sell their bonds back to the issuer at a premium (e.g. 101% of par value) when a specified event changes ownership/control of the company. This covenant has become increasingly complex due to the ease of adding additional conditions by the issuer (e.g. carve-outs for issuer). Additionally, certain CoC covenants are only triggered by specific events (e.g. rating downgrade, risky acquisitions).

- Coupon step-up – a coupon step-up covenant protects investors from credit risk by increasing coupon payments if the credit rating decreases. They are almost exclusively used on high-yield offerings where there is significant credit risk.

Generally, investment-grade issuers have few and simple covenants because of their size and relatively lower risk. High-yield issuers, on the other hand, typically agree to complex indentures with an extensive list of covenants due to their relatively higher risk.